I am an Assistant Professor at Toulouse School of Economics. My research falls at the intersection of industrial organization and finance. I apply a wide range of empirical methods, with a focus on using structural estimation to understand welfare implications of policies and market designs. In my current research, I create novel models to help understand how information frictions are generated in finance and technology industries, as well as how they affect competition and welfare. I completed my PhD in Economics at Boston University. Before joining TSE, I was a postdoctoral fellow at Tepper School of Business at Carnegie Mellon University.

Working Papers

Does Competition Between Experts Improve Information Quality: Evidence from the Security Analyst Market [New Draft Coming Soon]

[Draft]

Finalist for Young Economists’ Essay Award (YEEA) at EARIE 2021

Talks: NTU, SMU, IIOC, EARIE, FMA, BU Questrom, AFA (PhD Poster), BU, CMU Tepper, TSE, Oxford Saïd, ESSEC, OSU Fisher, Bank of Canada, Northwestern, NUS, Queen’s University, CEPR-JIE, Chicago Household Finance Conference, Econometric Society European Winter Meeting, HEC Paris, NHH, Econometric Society World Congress

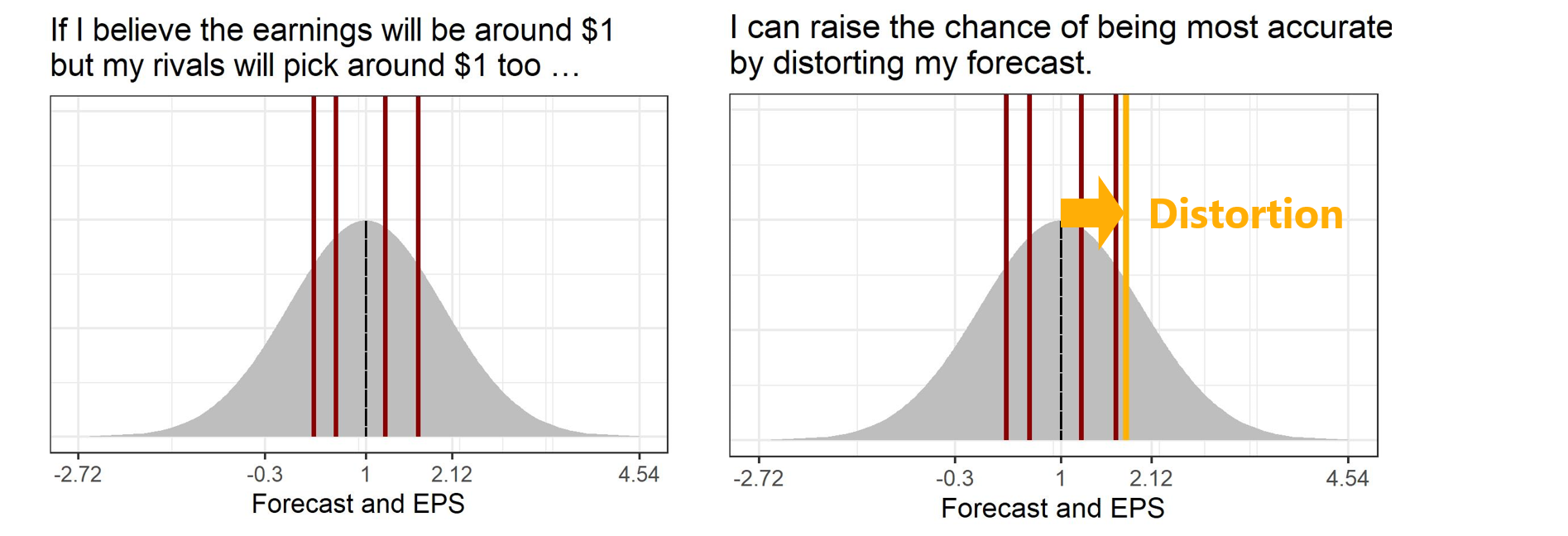

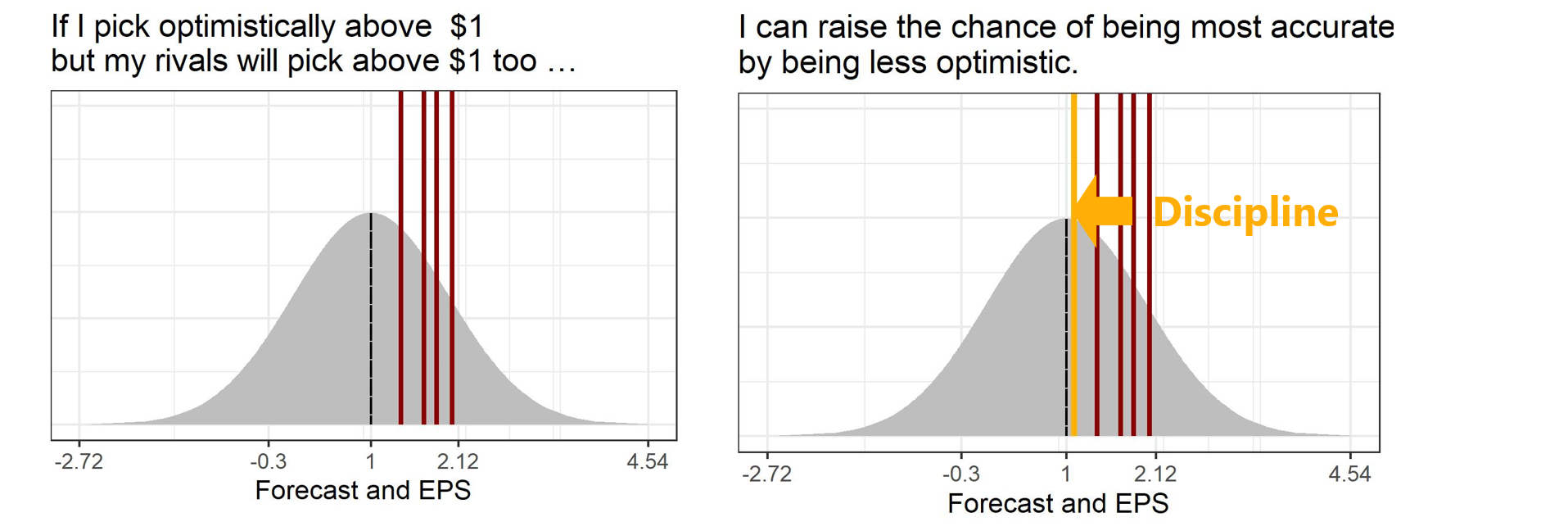

- Financial analysts are rewarded for being the most accurate. This leads them to distort their forecasts to differentiate themselves from their peers, but also disciplines their optimism bias. In the current market, the disciplinary effect dominates while both effects are present, so it is optimal to have moderate competition between analysts to both improve aggregate information and contain the distortion.

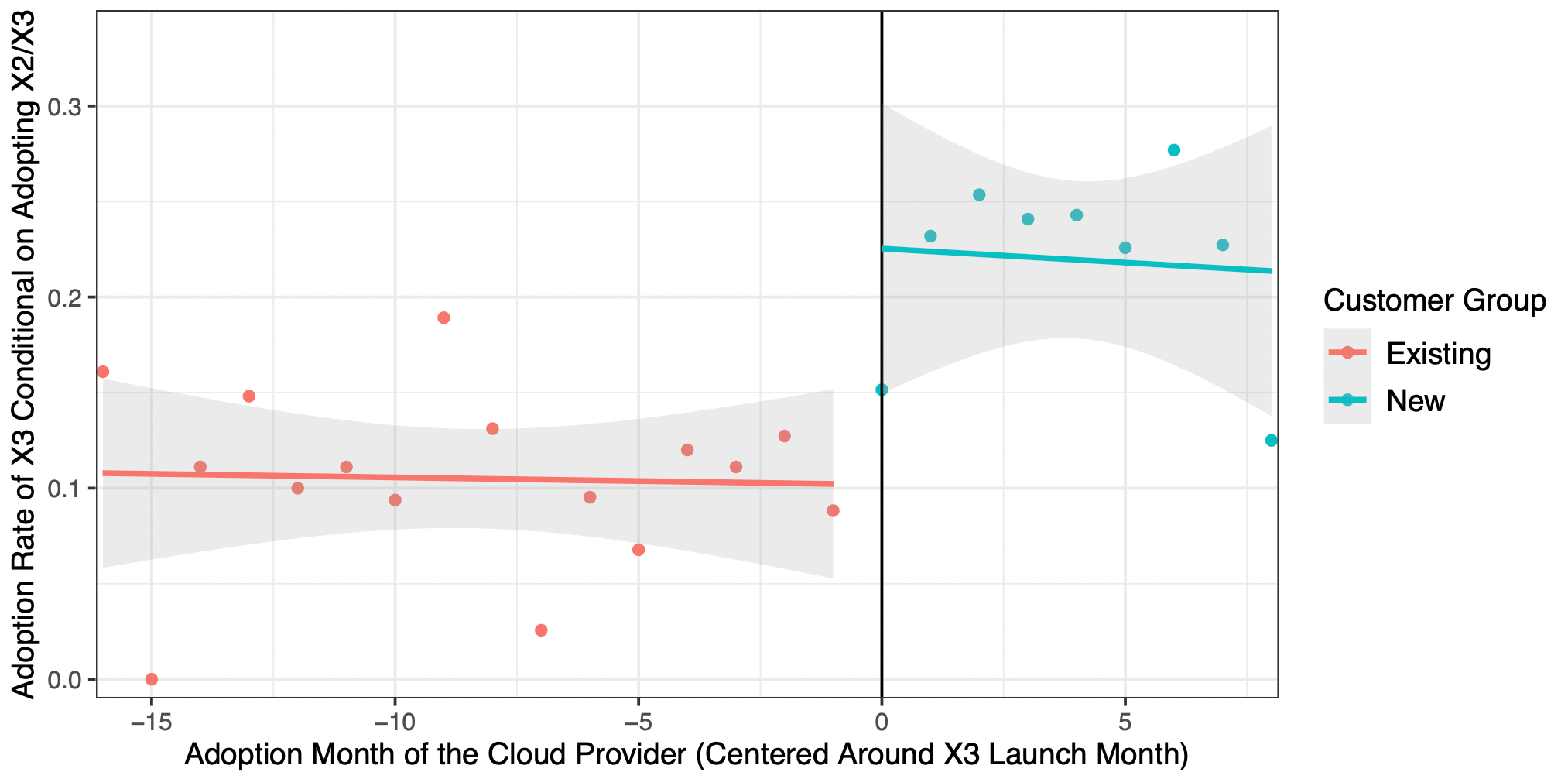

Firm Inertia in the Public Cloud [Latest draft: July 2026]

with Peichun Wang and Sida Peng

Previously circulated as Sticky Consumers and Cloud Welfare.

[Draft]

Talks: Boston University, EC’26, IIOC, NTU, Paris Dauphine Digital Regulation Workshop, Paris Digital Conference, Queen’s University, Toulouse Digital Economics Conference, Zhejiang University; by coauthor: AI and Economics Workshop, Microsoft, Jinan-SHUFE IO Conference, City University of Hong Kong, Hong Kong University of Science and Technology, University of Hong Kong

- Firms are slow to adopt better cloud products even in a ``best-case’’ switching environment where conventional technical and contractual frictions are minimal: within the same provider, data center, and product series. This inertia delays technology adoption and suppresses cloud usage, reducing both consumer surplus and provider revenue. Nevertheless, firms still derive substantial surplus from cloud use.

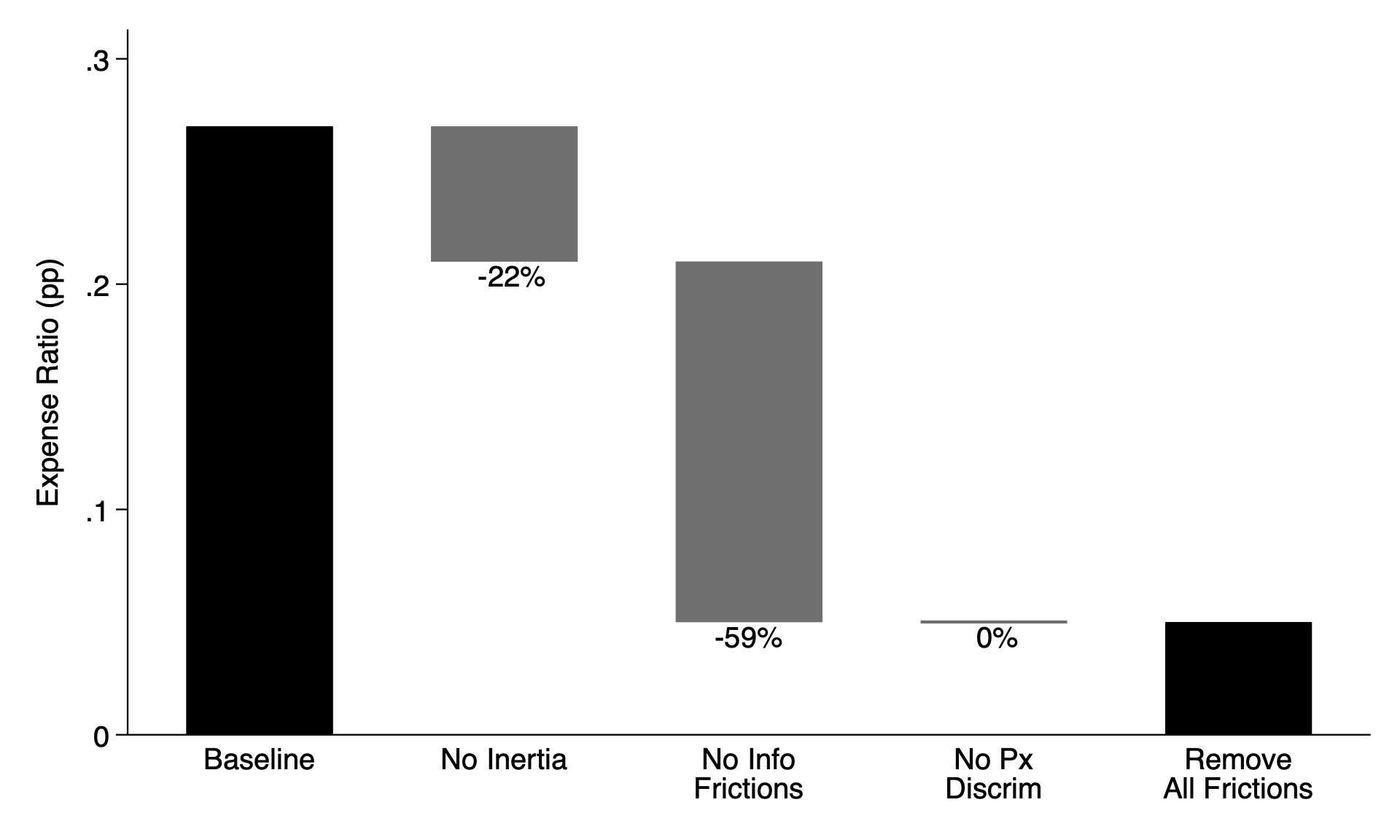

Why Do Index Funds Have Market Power? Quantifying Frictions in the Index Fund Market [Latest draft: July 2026]

with Zach Brown, Mark Egan, Jihye Jeon, and Alex Wu

[Draft]

Talks: Econometric Society European Meeting, IIOC, SMU, SITE, TSE, UCI, UCR, University of Chicago, WFA; by coauthor: American University, the Boston Conference on Markets and Competition, BU, CMU, LSE, the Montreal Summer Conference on Industrial Organization, Northwestern, OSU, Rice, Stockholm School of Economics, UCLA, the University of Florida, the University of Georgia, the University of Wisconsin IO/Finance Reading Group.

- Despite the proliferation of near-identical index funds, fee dispersion remains large and persistent. We develop a dynamic model of demand and supply featuring inertia, information frictions, and preference heterogeneity, using fund-level new-sales data to identify how often investors update their holdings. Only 3-5% of investors update each month. Eliminating inertia alone lowers average fees by about 20%, while eliminating both inertia and information frictions lowers them by about 80%, highlighting the importance of their interaction. ETF entry reduced expense ratios through lower costs and greater competition, but demand-side frictions substantially dampened these gains.

Why Multimarket Banks Exist: A Quantitative Theory With Demand Complementarity [Draft Available Upon Request]

with Jack Liebersohn and Yufeng Wu

Talks: Toulouse School of Economics, UIC Finance Conference, Fischer-Shain Center Research Conference (Upcoming); by coauthor: OSU Fisher, Chicago Fed, University of California at Irvine, University of Bristol, University of Exeter, SAIF, City University of Hong Kong, The University of Hong Kong, HKUST, Cheung Kong Graduate School of Business, PBCSF Tsinghua University, Econometric Society DSE Conference (Upcoming).

- Consumers prefer to obtain multiple financial products from the same bank. We first provide causal evidence of this demand complementarity in banking using a shift-share design exploiting local variation in Conforming Loan Limits. Then, we estimate a dynamic oligopoly model to study its implications for banks that operate in multiple markets, quantifying impacts on bank synergies, pricing strategies, and the interconnection of their services across markets.